Declining Economic Conditions: Impact on business valuation

Economies around the world have witnessed slow growth resulting from the spillover effect of the COVID-19 pandemic and economic restrictions.

The outbreak of the Russia-Ukraine war in February 2022 has made this situation worse by intensifying supply chain interruptions, raising the cost of food, energy, and other commodities.

Inflation has risen sharply around the world, prompting major central banks to raise policy rates. Rising policy rates began in the second quarter of 2021, when some central banks in Latin America and Central Europe focused on curbing inflationary pressures and the attendant impact on currency – when inflation increases, the purchasing power of money reduces. In other words, consumers can buy less goods with same amount of currency.

This trend has been sustained in 2022 as the U.S. Fed and other major central banks across the globe continue to increase rates at a pace faster than experienced in the last five decades.

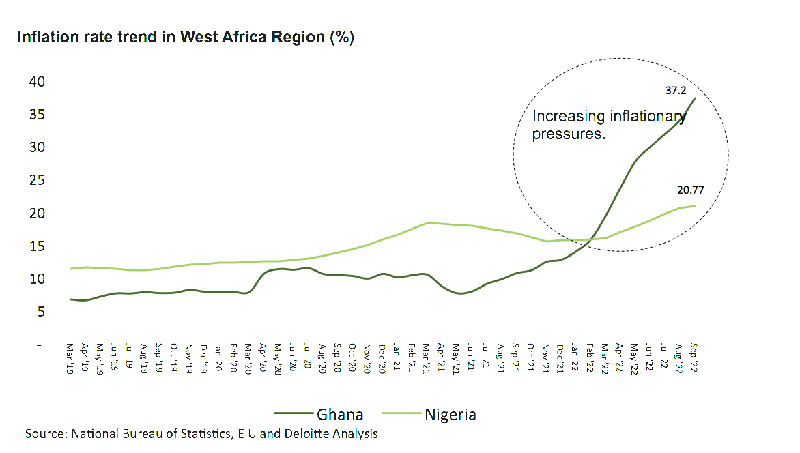

West Africaa is not excluded from the global economic challenges

Following recovery from the recession induced by the COVID-19 pandemic, key economic indicators such as inflation rates, policy rates and exchange rates have worsened in West Africa. For example, according to data from the National Bureau of Statistics in Nigeria, headline inflation rate has risen from 15.6 per cent in December 2021 to 20.8 per cent in September 2022, which represents a 17-year high. The high inflation rate is largely due to rising food prices, disruptions in the food supply chain, currency depreciation, insecurity, and high input cost. Consequently, the Central Bank of Nigeria (CBN) has adopted a tight monetary policy stance, raising benchmark interest rate to 15.5 per cent at its last policy meeting in September 2022, from 11.5 per cent at the start of the year.

We have witnessed similar macro-economic trends in Ghana as the headline inflation rate has risen from 12.6 per cent in December 2021 to 37.2 per cent in September 2022, reaching a 20-year high. The high inflation rate in Ghana is due to rising food and transportation prices, disruption in food supply chain as well as the persistent depreciation of the Cedi. The Ghana Cedi has depreciated by about 45 per cent against the U.S. dollar so far in 2022, with knock-on inflationary effects given Ghana’s high dependence on imports. As a result of the inflationary pressures, the Bank of Ghana (BoG) has maintained a contractionary stance, increasing interest rates to 24.5 per cent in October 2022, from 14.5 per cent at the start of the year.

Implication of rising inflation and interest rates on businesses

In the face of global inflationary pressures, nations are faced with conflicting priorities to maintain domestic price stability and ensure economic growth. The interest rate is one of the most important tools used by central banks to manage the flow of money and output. A change in interest rate has an overarching impact on the economy as well as other key economic indicators such as consumer spending and borrowing.

Rising inflation impacts businesses in other ways such as increased production costs and profitability margin erosion, especially where costs cannot be passed on to consumers. While most central banks have raised rates in response to this, the increased interest rate is supposed to help with reducing inflationary pressures, it affects firms cost of borrowing as debt becomes more expensive causing higher default rates. Increased costs of borrowing could also put a strain on the entities’ cash flow and there could be breach of key debt covenants contained in debt agreements.

Furthermore, rising interest rates tend to negatively affect stock markets, as they are a leading indicator for slow economic growth. For context, the U.S. equities markets (S&P 500 Index) has declined by 16.99 per cent in 2022 (as at November 2022) as the U.S. Fed has consistently raised benchmark interest rates from a range of 0 per cent - 0.25 per cent at the start of the year to 3.75 per cent - 4 per cent as at November 2022. Higher interest rates can have a negative impact on the future earnings of companies, especially those that rely on borrowings with potential impact on share prices as well.

Why impairment testing should be a key consideration

The core objective of International Accounting Standards (IAS) 36 is to ensure that an entity's assets are not carried at more than their recoverable amount i.e., the higher of Fair Value less Costs of Disposal (“FVLCD”) and Value in Use (“VIU”).

FVLCD represents the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date while VIU is the expected future cash flows that the asset in its current condition will produce, discounted to present value using an appropriate discount rate.

Entities are required to perform impairment tests when there is an indication that an asset is impaired, and the test may be carried out for a "cash-generating unit" when an asset does not produce cash inflows that are largely independent of those from other assets. However, goodwill and indefinite-lived intangible assets are required to be tested for impairment annually.

IAS 36 suggests that assets should be tested for impairment when there is an indication that the fair value of an entity (or a reporting unit) may be below its carrying amount. According to paragraph 12 of IAS 36, in assessing whether there is any indication that an asset may be impaired, an entity shall consider, as a minimum, the following indications:

• Decline in market value

• Negative changes in economy, technology, markets or laws

• Increase in interest rates

• Net asset of company higher than market capitalization

Based on the above, companies may be facing a higher risk of impairment driven by the rise in interest rates globally. Furthermore, the net assets of 42 per cent of corporates listed on the NGX were higher than their current market capitalization as of June 2022 (excluding financial services and real estate companies), indicating the possibility for impairment.

This is further corroborated by historical data as we observed a positive correlation between weak economic conditions and asset impairments recorded by corporate entities in Nigeria. The 2016–2017 high inflationary period provides context to the size of impairments recognized during unstable economic times due to the application of the standard. Our analysis reveals a high correlation between inflationary pressures and impairment losses as shown below.

Close relationship between key economic indicators and impairment recorded by corporate entities in Nigeria.

With rising concern around global economic conditions and the local economy, it becomes imperative for entities to test assets for impairment.

Our analysis excludes financial services and real estate companies as their balance sheets items are closer to fair value relative to other companies.

Due to limited data, we are unable to show this relationship for other West African countries.

Companies in Nigeria and Ghana are currently facing the triple challenge of rising inflation, rising interest rates and persistent currency depreciation which present short to medium term risks for majority of businesses. Some of these risks include but are not limited to:

• Dwindling margins resulting from input cost pressures, especially when this cannot be passed to customers

• Higher cost of capital and limited incentive to invest in longer term capital projects

• Foreign exchange losses (relating to companies that import their inputs)

• Pressures on revenue and profits following erosion of purchasing power

Consequently, in order to properly comply with the requirements of the International Financial Reporting Standards, it is important that assets should be tested for impairment regularly.

Economic indicators and impact on business valuation

Economic conditions have critical impact on business valuation and inflation plays an important role in a company’s financial situation, influencing how investors and professional valuers’ approach corporate valuations. An analysis of the 2022 performance of stock exchanges around the globe demonstrates how investors are looking at profitability and how they value businesses in tough economic environments.

Relationship between interest rate and market performance

Periods of economic instability usually usher in weak consumer confidence. Consumer confidence is another important factor affecting the demand for consumer goods and overall profitability of a business. During times of economic buoyancy, consumers are more likely to purchase higher amounts of goods and services as they feel confident about the economic outlook and their personal finances. This bodes positively for businesses as revenue grows faster.

However, during high inflationary periods, businesses face higher input costs resulting to weaker margins. Since the discounted cashflow model derives the value of a company based on the amount of cash/income remaining after the entity has settled all the cashflows required to run its operations, working capital and capital expenditure, declining margins impacts stock price and business valuation adversely. Therefore, business value is eroded when the economic outlook is gloomy.

The cost of running business operations (rent, utilities, cost of production) rises as inflation increases. This becomes another constraint for business owners as they must consider strategies to transfer higher cost to customers, if and where possible. If costs reach unbearably high levels without proportionate rise in revenue, the company’s valuation is impacted. The table below shows the impact of rising inflation and interest rate on business valuation.

Impact of rising inflation and interest rate on business valuation

All other things being equal, rising inflation affects total revenue negatively as increase in prices of goods and services leads to reduced demand by customers. However, businesses that produce and sell inelastic goods and services (such as consumer staples and utilities etc.) may not be affected by rising inflation as the demand for such goods and services are less sensitive to price changes.

For customers that depend on borrowing for consumption, rising interest rate leads to higher borrowing cost thereby negatively impacting volume of goods and services they can purchase. This means businesses will record lower sales, reducing overall business revenue.

Lower revenue affects business valuation, VIU and FVLCD negatively as this is likely to lead to lower net income and free cash flows.

Operating cost

Inflationary pressure can lead to increased costs for businesses including labor, materials, overhead, and energy. Companies that are unable to transfer higher costs to customers through higher prices would face the issue of lower profitability.

Higher operating costs without a corresponding increase in revenue has a negative impact on business valuation. This is because costs represent outflows to the company and a deduction from revenue, hence a reduction to the firm’s free cash flows.

A discount rate is a rate that is used to determine the present value of future cash flowsb. It may be referred to as the company's cost of capital (debt and equity). Discount rates are typically calculated using the Capital Asset Pricing Model (CAPM) and Weighted Average Cost of Capital (WACC) formulae as a starting point, therefore, combining different elements including the risk-free interest rate and equity-risk premium. There is a negative relationship between discount rate and the overall value of the discounted cash flow model as such higher discount rates leads to lower business value, VIU and FVLCD. This also applies to the valuation of assets tested for impairment, including intangible assets like goodwill. Updated business strategy plans aimed at improving cash flow assumptions will be necessary to counterbalance this decline in value; otherwise, there is a higher likelihood of impairment. We have discussed how rising interest rates and inflation impact each component of discount rate below:

Risk-free rate: Risk-free interest rates are the foundation of discount rate calculations used in discounted cash flow models. The risk-free rate is the rate of return on an investment with zero riskc. The rate usually moves in the same direction with inflation and benchmark interest rate because interest rates are the primary tool used by central banks to manage inflation. As such, all other things being equal, higher risk-free rates lead to higher discount rates and vice versa.

Country risk premium: Country Risk Premium (CRP) is the additional return or premium demanded by investors to compensate them for the higher risk associated with investing in a riskier foreign country, compared with investing in a less risky domestic market.

There are three methods of calculating CRPc:

• Default spread of country: This method calculates CRP for a specific country by comparing the spread on sovereign debt yields between the country and a mature market, such as the United States.

• The equities volatility-based technique calculates CRP based on the relative volatility of equity market returns between a certain country and a developed country.

• A hybrid approach that combines the above two methods.

All other things being equal, when using the default spread approach to determine CRP, a higher interest rate could imply a higher country risk premium and vice versa, since interest rate have a positive relationship with bond yields.

Furthermore, since higher interest rate negatively affects earnings and share prices as future earnings from shares become less attractive when compared to bond yield, it is arguable that higher interest rate environment can account for higher equity volatility of the local equity market when compared with the developed market (assuming the developed market is experiencing stability). Consequently, higher interest rate is expected to result in increased CRP, all other things being equal.

Equity risk premium: Equity Risk Premium (ERP) is the excess return earned by a stock market investor over a risk-free rate. Depending on how it is measured, equity risk premium could have a positive relationship with interest rate. While this relationship may vary over time, we have observed how ERP has risen with interest rate since 2021.

Cost of debt: Cost of debt simply refers to the company’s cost of borrowings i.e., the return that a company provides to its creditors and borrowers. It is usually derived by adding a spread over the current risk-free rate to account for the default risk related to the entity raising the debt. As such, a higher risk-free rate leads to higher cost of debt.

Based on the above, we expect a higher discount rate in a rising interest rate/inflationary environment, implying a lower business value, VIU and FVLCD. Hence, the likelihood of impairment loss is increased when recoverable amount is compared with the assets’ carrying amount.

Final Conclusions

It should be noted that a rising inflationary environment may lead to cashflow adjustments to ensure that discount rates and the cash flows are consistent and comparable. Where cash flows reflect current inflationary environment (cash flow in nominal terms), the discount rate adopted should include effects of inflation (nominal rate) and vice versa.