Fiscal monitor: Fiscal policy in the great election year

Amid mounting debt, now is the time to bring back sustainable public finances. As prospects for a soft landing have improved, especially in the United States, policy uncertainty has declined and risks around the world economic outlook are becoming better balanced (April 2024 World Economic Outlook).

Inflation has fallen quickly in recent months, leading to an optimistic mood in financial markets. Markets seem convinced that most of the road to restoring global price stability is behind us, allowing major central banks to gradually ease monetary policy rates in coming quarters (April 2024 Global Financial Stability Report).

Sovereign bonds spreads have narrowed, and countries in sub-Saharan Africa, which had been inactive in international capital markets since mid-2022, resumed bond issuance in early 2024.

After jumping to record levels in 2020—as part of the response to the COVID-19 pandemic—deficits and debt fell sharply in 2021 and 2022. Bu they increased in 2023, pausing progress toward normalization.

In 2024, overall deficits are projected to narrow again. Nevertheless, four years after the onset of the pandemic, public debts and deficits are higher and debts are projected to remain high. Chapter 1 of the Fiscal Monitor documents divergences in fiscal policies around the world.

Global public debt

First, the projected rise in global public debt is mainly driven by China and the United States, where public debt is now higher and expected to grow faster than pre pandemic projections.

Fiscal policy developments in these major economies, notably in the United States, have implications for global financing conditions. In many other countries, fiscal policy is projected to reduce or to stabilize public-debt-to-GDP ratios, though at levels higher than before the pandemic.

Yet primary deficits will remain above debt-stabilizing levels in 2029 under current projections in more than one-third of advanced and emerging market economies and more than one-quarter of low-income developing countries.

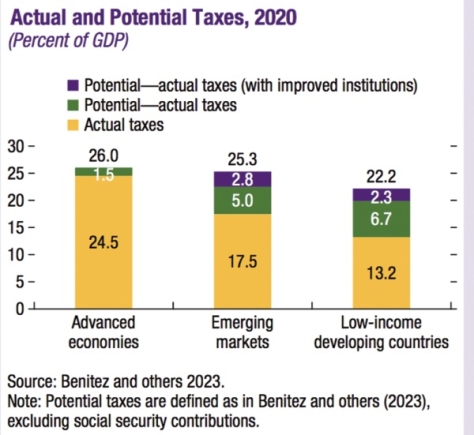

Another divergent trend affects low-income developing countries. It is in these countries that scarring from the pandemic is most significant. It is also in these countries that financing is most scarce, shaping the evolution of deficits and debt.

Policy space

These severe limits on policy space limit the ability of the state to support growth and development.

Six months ago, the Fiscal Monitor emphasized the policy trilemma associated with, first, strong spending pressures on national budgets—including from wages, pensions, health care, industrial policies, the environment, defense, and Sustainable Development Goals; second, political resistance to taxation; and third, the need to contain debt and deficits to deliver fiscal sustainability and financial stability.

Now, higher interest rates and lower medium-term growth prospects add to the more challenging debt dynamics. Furthermore, the risks of fiscal slippages are particularly pronounced this time around.

In fact, 2024 is the year when the political aspect of the policy trilemma described here will exert a heavy influence, in the form of the Great Election Year.

Eighty-eight countries have already held or will hold elections this year. Empirical evidence points to a bias toward fiscal slippages in elections years. And this time, the political discourse is particularly loud in favor of fiscal expansion.

Fiscal consolidation

In this context, durable and credible fiscal consolidation is needed to reestablish sound public finances, to build budgetary space for priority investments, and to deal with future shocks.

Tackling debt and deficits today helps to avoid more painful adjustments later. Fiscal tightening would also be an important contribution to completing the last mile of disinflation (especially in economies characterized by excess demand).

But while domestic resource mobilization—including strong tax capacity, state capacity, and a mature domestic public debt market—favor sustainable development, they are far from sufficient. And, in the absence of economic growth, even sound public finances will be eventually undermined.

In the long run, economic potential is mainly driven by productivity growth. And productivity growth, in turn, is driven by the production and diffusion of innovations.

Should we welcome or fear potentially disruptive innovations such as generative artificial intelligence?

On one hand, we should welcome them, as they could generate a cascade of societal transformations that drive growth and development.