Elections pose no major risks but IMF thinks otherwise

The December 7 elections do not pose any major risks to Ghana’s economic rebalancing or its ability to implement the economic stabilisation and reform programme backed by the International Monetary Fund (IMF), a new report issued by Standard Bank Research has stated.

Advertisement

The report, which is based on a review of Ghana’s economy said unlike the 2012 elections when President John Mahama needed to be marketed strongly, the current government did not appear to be under any pressure to boost expenditure in order to secure victory at the polls and was, therefore, delivering on the IMF programme.

“After many years of significant currency weakness, a widening current account deficit, persistent fiscal challenges and high levels of inflation amidst key structural bottlenecks, Ghana appears to be showing signs of economic rebalancing.

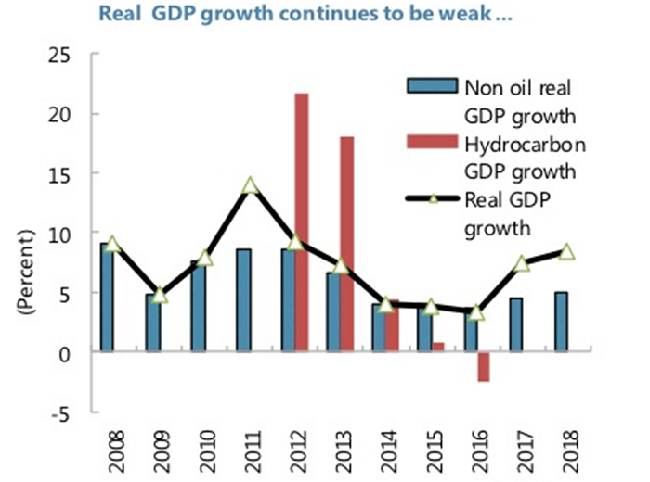

The report, African Markets Revealed, stated that although the country’s real GDP growth, which slowed from 14.1 per cent in 2011 to 3.9 per cent in 2015, was now likely to consolidate around 4.5 per cent at the end of the year, before it would accelerate to six per cent in 2017, as oil production picks up.

On the contrary, the IMF in its Country Report on Ghana sees the elections as a major risk to its programme with Ghana and said it would require continued strong policies and reform execution throughout to the upcoming election period, with tighter financing conditions.

It also wants the government to be highly transparent in order to subdue risk averse investors who may want to hold back, due to election outcome uncertainties.

But, the IMF also sees a higher growth of about 7.2 per cent of GDP in 2017, based on additional oil production and exports.

Last week, Mr Alhassan Andani, the Managing Director of Stanbic Bank, a member of the Standard Bank Group, said investors with eyes on investment opportunities in Ghana should sink their investments now, as the economy readies to move into higher growth mode from next year in view of tough decisions that had been taken to achieve fiscal consolidation.

His assertions were corroborated by the Senior Country Partner of Accounting and Advisory firm, PricewaterhouseCoopers (PwC), Mr Vish Ashiaghor.

Although the government cut its 2016 growth expectations to around 3.5 per cent based on interrupted oil production after an oil floating production, storage and offloading (FPSO) unit became damaged, the IMF is more optimistic based on expected additional oil inflows as the Tweneboa, Enyenra and Ntomme (TEN) fields started pouring oil in August.

The IMF optimism is also informed by improvements in the country’s power situation as positive developments that should lift growth in the period ahead.

At the back of higher oil production from TEN, Standard Bank also expects the country’s foreign exchange (FX) position to improve which could result in higher government and private sector consumption spending.

“While we expect private consumption to improve over the next year or so, we suspect that as a share of overall GDP, it should reduce slightly over the medium term as investment spend potentially takes a larger share.

“Indeed, on-going investments in the natural gas sector and potential increases in power-related investments should boost expenditure on domestic capital formation in the coming years,” the report suggested.

Risks to growth

The economy already lags behind infrastructure delivery, leaving a large funding gap. Financing the infrastructure could be hampered by the on-going fiscal consolidation efforts which in the near term may not support growth in the economy.

“All said, we are aware that a sizeable infrastructural and funding deficit still exists and the government’s plans could limit the space for significant infrastructural spending which may limit any sustained upside to real GDP growth in coming years,” the report stated.

Election headwinds

The Standard Bank report, which is largely used by its clients, offshore partner banks, institutions and potential investors in Africa, does not see any major risks posed by the December 7 elections because it believes whatever the outcome of the election would not lead to a discontinuation of the Extended Credit Facility (ECF) backed IMF bailout programme.

The review points out that although the main opposition leader, Nana Akuffo Addo of the NPP, had accused the current administration of not doing enough to improve consumer and business conditions, “we suspect it will not be enough to tilt the election in his favour.”

In any case, the review posits, “we do not expect a huge departure from current economic policies and support for the IMF programme regardless of who wins the elections in December 16.”

This is because unlike the previous elections, the current government did not appear to be under any pressure to boost expenditure in order to secure victory at the polls.

“Also, while some might argue that the austere fiscal and monetary policies which have been introduced in a bid to restore macroeconomic stability may have proven unpopular, we suspect that this has predominantly impacted urban dwellers, with rural areas potentially still firmly beholden to the NDC,” the report stated.

On the contrary, the IMF fears the elections posed major risk to its programme with Ghana, but warns that with an already much higher public debt level, a repeat of election year fiscal slippage could lead to a full-blown economic and financial crisis for the country and undermine development progress.

Should that not happen, another hurdle to the economic rebalancing remains an election-related heightened risk aversion and investor uncertainty. The IMF said the way to go around that was for the government to sustain fiscal transparency and be ready to tighten policies aggressively as the situation may demand.

“In the context of the now much higher public debt level, a replay of the past spending splurges in election years would greatly heighten the risk of a full-blown economic and financial crisis and undermine Ghana’s development progress. Even absent such a policy slippage, heightened risk aversion and investor uncertainty as the December 2016 election approaches could yet pose a challenge,” the IMF stated in its 121-page Report on Ghana issued earlier this month after its third review in last month.

The President, John Dramani Mahama and his Finance Minister, Mr Seth Terkper, have given assurances at different fora that they would stick to the fiscal plan and would not over-spend in an election year to derail any gains made.

Balance of payments

Standard Bank sees oil production as playing a major role in Ghana’s economy for the rest of the year, up to 2017. The balance of payment position worsened from a deficit of 1.1 per cent of GDP in March this year to 1.9 per cent at the end of June 2016. The balance of trade gap also widened from 1.7 per cent of GDP deficit in March this year to 3.4 per cent deficit as of end June.

The report traces the worsening position to 60 per cent fall in oil export revenue and a marginal increase in non-oil imports, but believes export volumes may recover modestly in the second half of the year with the coming on stream of TEN as well as improvements in the condition of FPSO Kwame Nkrumah.

It, however, sees a further widening (slightly though) in the trade balance on account of lower cocoa production and only a marginal increase in non-oil exports before the end of the year.

What the Standard Bank report did not take into account, however, is that election years in Ghana are characterised by somewhat disruptions in festive occasions such as Christmas and Eid which slow economic activity, and hence subdue imports.

The report is spot on, however, arguing that the addition of around 80,000 bpd of oil exports should substantially improve the trade balance and consequently the current account deficit in 2017.

“As a result, we expect that the current account deficit will widen slightly in 2016 to about US$3 billion (7.2% of GDP) but narrow to about US$1.5 billion (3.2% of GDP) in 2017 due to new oil production. Another break in production at the FPSO in order to find a permanent solution to its damaged bearings as well as an expected ramp-up of import demand may slow down the pace of contraction in the C/A deficit.”